|

| Magazine |

|

| About |

|

| SUMMIT |

|

| Contacts |

|

| Home |

|

|

|

|

|

| |

|

|

|

| #3' 2002 |

print version |

RENOVATION OF POWER INDUSTRY STARTS IN ST. PETERSBURG |

|

Gennady Voskresensky

|

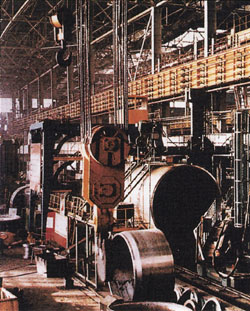

Leningradsky metal works is making rotors for thermal power turbines |

As soon as Russia’s economy started showing signs of growth, industrialists had to pay closer attention to the state of the country’s power system and ask themselves a question, if there was any potential for its modernization.

It turned out that the answer was positive. Power engineering enterprises were prepared to participate in modernizing the power system. In the years of Russia’s economic crisis they in no way lost their traditionally solid production positions. On the contrary, they managed to even strengthen them. In some segments of the world’s market the share of Russian manufacturers accounts for 8 % to 11 %, despite the severe competition, which is going on in power engineering because of existing redundant capacities.

Not long ago, just in the early 1990s, the Russian power engineering industry was assigned an auxiliary role. But now, more often than not, the world’s largest concerns, such as Siemens, General Electric, Toshiba, ABB, Hitachi, Skoda, recognize Russians as serious competitors and are readily establishing partnership relations with them through joint strategic projects.

All this forms a good basis for their participation in federal program «Russia’s energy strategy for the period till 2020». The document worked out by the Russian Ministry of Energy and members of the Russian Academy of Sciences provides for a radical upturn in this field that should contribute to advancing the power engineering industry and allied sectors of the country’s economy: metals industry, metal working, etc.

Practically all Russian power engineering enterprises (there are more than 50 of them) are involved in implementing the program. The largest high-capacity ones are based either in St. Petersburg or close to this city, which is often called Russia’s northern capital. Among them are joint-stock companies Leningradsky Metal Works, Elektrosila Plant, Turbine Blade Plant, Izhorskiye Zavody, Novaya Sila, Zvezda, Baltiysky Works, etc. Their share amounts to almost 70 % of the industry’s total production volume.

Each of these enterprises has good prospects for getting major contracts since the fuel-and-energy complex is expected to implement a large-scale replacement of existing equipment. For example, in Russia, like in other CIS countries, over 60 % of steam turbines have been in operation for no less than 30 years. About 90 % of equipment at power-generating units of thermal power stations have exhausted their calculated resources and should be either replaced or overhauled. Most of 29 power-generating units in the nuclear power industry are approaching the end of their designed operation life. Four blocks have already been stopped and are now being prepared to be put out of operation. At least 15 more power-generating units are to be stopped and modernized by 2010.

Contracts from the fuel-and-energy complex, and the nuclear power industry in particular, will replenish the portfolio of the power engineering industry emptied in the early 1990s with the completion of delivering basic production equipment to those installations, which are now out of operation. The Russian Ministry for Atomic Energy intends to annually construct one power-generating unit for new nuclear power plants starting from 2003. If these ambitious plans are to be implemented, power engineering enterprises will be able to considerably expand their presence in the domestic market. Besides, in the nearest 6 years they will have to do a lot of work for exports. Leningradsky Metal Works, Elektrosila Plant and Izhorskiye Zavody are already participating in construction of power-generating units for Chinese, Iranian and Indian nuclear power plants. The value of export orders for this period is estimated at $1.4 billion. Political factors played a major role in forming such a large portfolio: Russia is providing equipment for nuclear power plants in those countries that foreign competitors refuse to cooperate with.

This created favorable conditions for power engineering enterprises in Russia’s North-West. The last two years were quite a success for them. Proceeds from sales increased considerably. At the same time Elektrosila and Izhorskiye Zavody registered an improvement of ROS, the return on sales index. Both of them along with Zvezda JSC showed the surge in profitability of their assets and ownership capital as well as in earnings per share. These enterprises boosted the level of labor productivity, which is high for the Russian industry as a whole. In 2001 rates of production growth averaged 180 % as compared with 2000. This trend is still around in 2002 as well.

Meanwhile, all enterprises of the industry have got large payables and receivables (both short-term and long-term). Excessive liabilities have a negative impact on their financial stability, liquidity and business activity.

Facing these problems Silovye Mashiny, the power engineering concern, started paying more attention to implementation of the cooperation agreement reached in 2000 with Vneshtorgbank and Rosbank, Russia’s two major banks. The agreement provides for setting up additional sources of financing to develop production as well as for opening credit lines and arranging syndicated bank credits, drafting joint investment projects and leasing programs.

Analysts think it probable that in the next 5 to 10 years power engineering companies will be dynamically developing. The financial base for this will be secured by direct and portfolio investments as well as by bank credits. It is not ruled out that along with the increase of business portfolios companies’ net profit will also rise and that the priority will be given to developing production when distributing the profit.

|

Power engineering is one of the basic segments of Russia’s industry. There are more than 50 largest enterprises. The geography of their locations spans the North-West (St. Petersburg, the Leningrad and Arkhangelsk regions), the Urals and Volga-river region, Siberia. The North-West is represented by Leningradsky Metal Works, Elektrosila Plant, Turbine Blade Plant, Izhorskiye Zavody JSC, Novaya Sila , Zvezda Plant, Baltiysky Works, Power Engineering Plant JSC, State-owned Pilot Plant, Pellamash JSC, VNITI JSC, State-owned Unitary Northern Engineering Enterprise (Sevmash), State-owned Unitary Enterprise Zvezdochka, Solombalsky Power Engineering Plant JSC and others. The Urals and Volga-river region boast of Drilling-and-Metallurgical Equipment Plant JSC, State-owned Izhevsky Electromechanical Plant, Izhneftemash JSC, Kazanskoye Motor Engineering Association, Kirovsky Engineering Plant Krasny Proletary JSC, Kungursky Engineering Plant JSC, Vorovsky Engineering Plant JSC, Orsky Engineering Plant JSC, Pavlovsky Mashinostroitel JSC, Privod JSC, Reducer JSC, Uralgidromash JSC, Uralsky Compressor Plant JSC. Siberia has got Barnaultransmash JSC, State-owned Krasnoyarsky Engineering Plant, Tomsky Vakhrushev Electromechanical Plant JSC, Tyumenskie Motorostroitely JSC. Among enterprises in other regions are Chekhovsky Power Engineering Plant JSC (Moscow region), Elektropribor JSC (Vladimir region), Tulamashzavod JSC and Yasnogorsky Engineering Plant JSC (Tula region).

| |

| |

|

At present, export contracts account for 30 % to 50 % of business portfolios. It is probable that this ratio will remain unchanged. Orders from abroad are more attractive for enterprises since the stable yield in freely convertible currency serves as a certain guarantee against financial risks. However, the industry cannot afford to completely focus on exports because the equipment it manufactures is considered strategically important for the country’s economy. Power engineering enterprises are turning out basic and accessory equipment for thermal, nuclear, hydraulic and gas-turbine power plants. They fully satisfy needs of the Russian energy system, which is truly gigantic.

Steam turbines made by Leningradsky Metal Works and installed at Russia’s power plants account for 55 % of the total installed capacity of thermal and nuclear power plants. Elektrosila’s generators account for 80 % of installed capacity of Russia’s thermal power plants (60 % in the CIS), for 90 % and almost 100 % of capacities of hydraulic and nuclear power plants accordingly. Electric motors with Elektrosila’s trademark are used by more than two-thirds of Russian metals, metal working, shipbuilding, chemical, oil- and gas-producing enterprises. United Engineering Plants, which incorporates Izhorskiye Zavody JSC, is manufacturing equipment for the nuclear power and allied industries.

|

Manufacturing of equipment for a nuclear power plant at Izhorskie Zavody |

Experts at the State Duma, the lower house of the Russian Parliament, are convinced of the necessity for the State to take measures for protecting the industry. Among them are benefits for those power companies, which will give preference to Russian-made equipment when retooling, as well as State investments in capital assets and R & D at Russian power engineering enterprises. They believe that such measures will contribute to reorienting them on the domestic market. Besides, the State can introduce restrictions on exporting power engineering products by setting quotas and other limits through existing laws.

A rather serious problem is an inability of many companies to fulfill consumers’ orders on the turnkey basis. They have to act through State intermediaries, who determine exchange and finance terms in talks with contracting parties. Commissions for this kind of service amount to 3% to 14%. Very often intermediaries block up a considerable amount of current capital, make serious blunders in marketing. It is clear that all this undermines competitiveness of the industry’s enterprises.

Integration processes in the industry could be an alternative to strengthening of the state control. Manufacturers of power engineering equipment have already recognized advantages of integration, which ensures growth of labor productivity, business expansion and diversification as well as contributes to consolidating their bargaining positions. The successful integration is well illustrated by Silovye Mashiny set up in late 2000 and early 2001 on the initiative of InterRos holding company and a group of enterprises’ managers. The concern incorporated joint-stock companies Leningradsky Metal Works, Elektrosila Plant, Turbine Blade Plant and Kaluzhsky Turbine Plant. This became the first step in forming a united production structure of the power engineering industry. These companies will get their first experience of constructing power plants on the turnkey basis in India and this will signify the group’s achievement of strategic importance. They will be just one step away from securing serious investments in the industry.

The establishment of Silovye Mashiny Concern made a splash of interest among portfolio investors in the power engineering industry. Already in February and March of 2001 shares of Elektrosila JSC went up 104.75 % and shares of Leningradsky Metal Works JSC rose 67.66 %. The demand for shares of Izhorskiye Zavody JSC also jumped up with their price increasing by 110.53 %.

Nevertheless, stocks of Russian power engineering companies do not enjoy the blue-chip status so far. Like before, stock exchange experts keep putting them in «the second echelon». There is still much work to do and, above all, by emitters themselves, who are not too much concerned about quotations of securities being in circulation. Companies’ bosses are not inclined to regard the stock market as a source of investments. They trust bank credits more. So, there is an obvious conflict of interest between shareholders and enterprises’ managers. Trading shares comes to redistribution of blocks among a narrow group of stock market players. In his turn an investor is afraid of buying «a pig in a poke» since he is unable to adequately assess financial results of an emitting company, which often conceals them trying to avoid paying taxes. Also to this end many emitters form affiliated structures numbering in dozens. Investors are scared away by constant fights for controlling ownership inside companies.

As a whole, stocks of Russian power engineering enterprises are obviously undervalued. This becomes particularly evident when comparing their present financial and economic state with results for 1997, when prices of the industry’s corporate securities reached their peak values. Experts make the same conclusion by comparing the value of Russian companies with the value of their foreign peers.

Despite numerous difficulties being experienced by each individual enterprise, analysts’ predictions look optimistic: in the nearest 5 to 10 years the power engineering industry will be stepping up production volumes and this will undoubtedly mean the inflow of investments.

|

|

|

|

current issue

previous issue

russian issue

|

|

back

back